Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at AZZ (NYSE:AZZ) and the best and worst performers in the commercial building products industry.

Commercial building products companies, which often serve more complicated projects, can supplement their core business with higher-margin installation and consulting services revenues. More recently, advances to address labor availability and job site productivity have spurred innovation. Additionally, companies in the space that can produce more energy-efficient materials have opportunities to take share. However, these companies are at the whim of commercial construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of commercial building products companies.

The 5 commercial building products stocks we track reported a slower Q3. As a group, revenues missed analysts’ consensus estimates by 5.6%.

Thankfully, share prices of the companies have been resilient as they are up 5.1% on average since the latest earnings results.

AZZ (NYSE:AZZ)

Responsible for projects like nuclear facilities, AZZ (NYSE:AZZ) is a provider of metal coating and power infrastructure solutions.

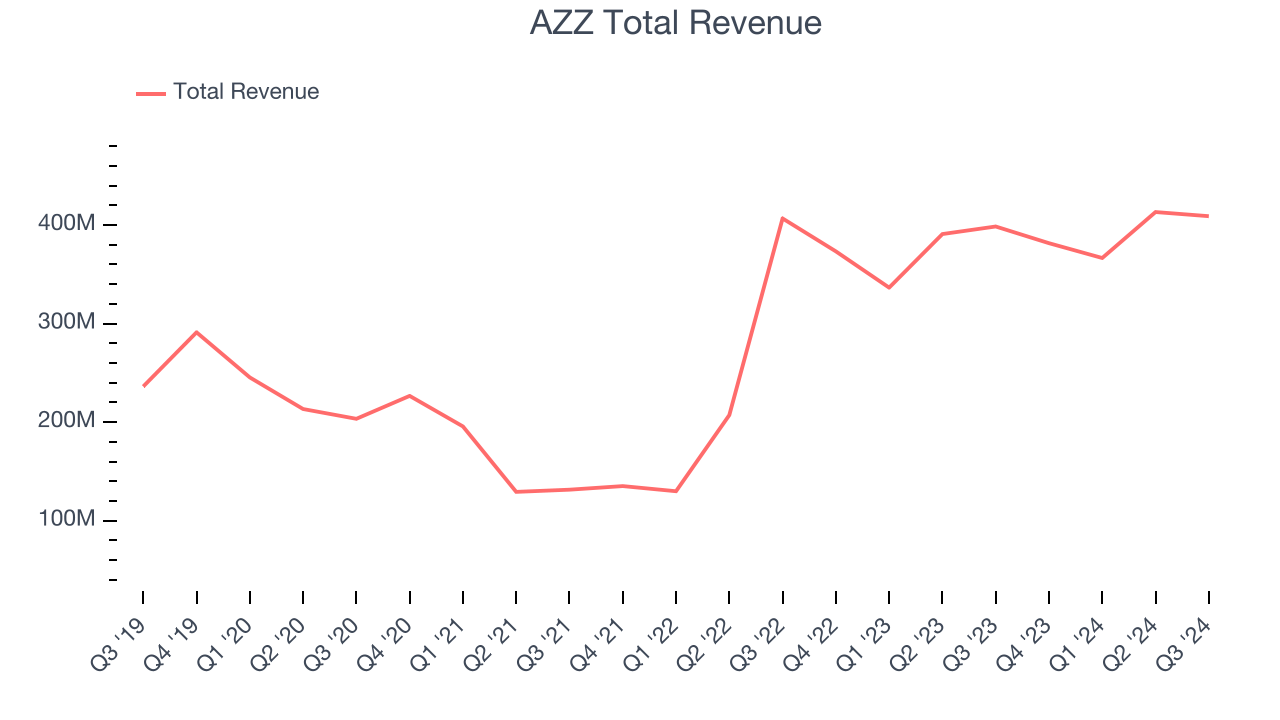

AZZ reported revenues of $409 million, up 2.6% year on year. This print fell short of analysts’ expectations by 0.7%. Overall, it was a slower quarter for the company with full-year revenue guidance missing analysts’ expectations.

AZZ scored the highest full-year guidance raise of the whole group. Unsurprisingly, the stock is up 17.4% since reporting and currently trades at $95.69.

Is now the time to buy AZZ? Access our full analysis of the earnings results here, it’s free.

Best Q3: Apogee (NASDAQ:APOG)

Involved in the design of the Apple Store on Fifth Avenue in New York City, Apogee (NASDAQ:APOG) sells architectural products and services such as high-performance glass for commercial buildings.

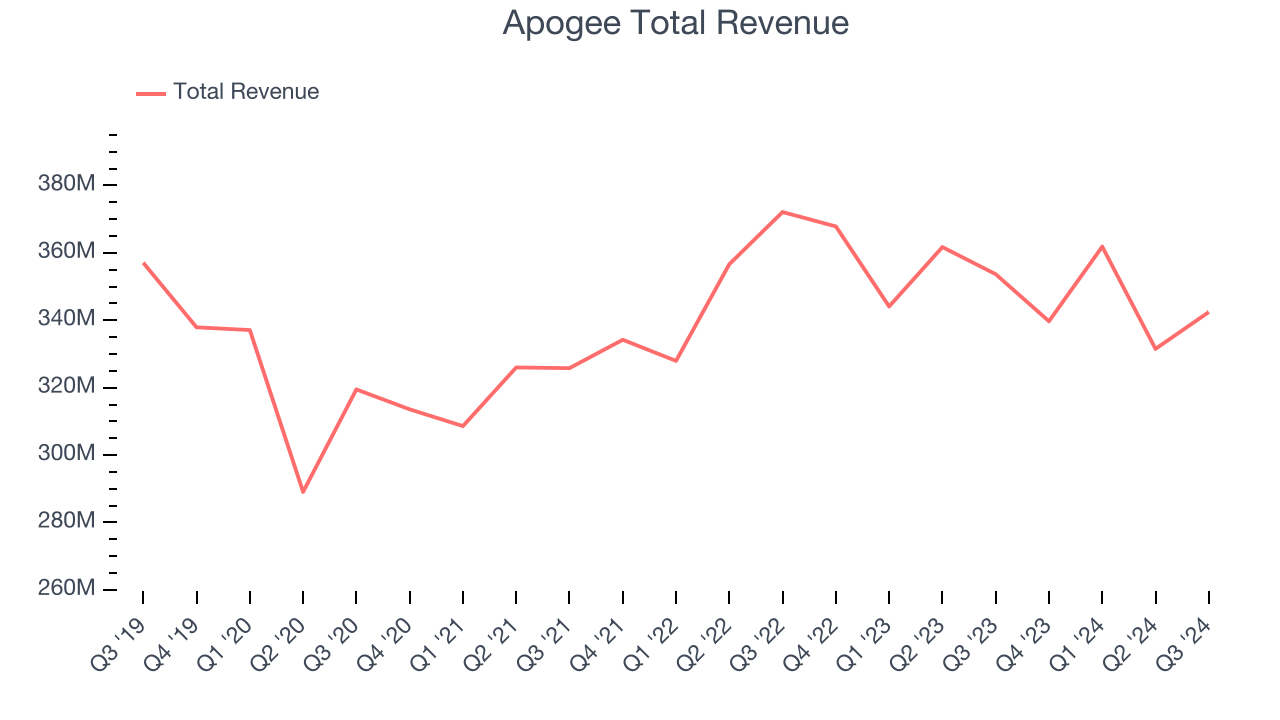

Apogee reported revenues of $342.4 million, down 3.2% year on year, outperforming analysts’ expectations by 2%. The business had a stunning quarter with an impressive beat of analysts’ EBITDA estimates and full-year EPS guidance exceeding analysts’ expectations.

Apogee pulled off the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 22% since reporting. It currently trades at $83.50.

Is now the time to buy Apogee? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Janus (NYSE:JBI)

Standing out with its digital keyless entry into self-storage room technology, Janus (NYSE:JBI) is a provider of easily accessible self-storage solutions.

Janus reported revenues of $230.1 million, down 17.9% year on year, falling short of analysts’ expectations by 7.3%. It was a disappointing quarter as it posted full-year revenue guidance missing analysts’ expectations.

Janus delivered the slowest revenue growth and weakest full-year guidance update in the group. As expected, the stock is down 26.8% since the results and currently trades at $7.55.

Read our full analysis of Janus’s results here.

Insteel (NYSE:IIIN)

Growing from a small wire manufacturer to one of the largest in the U.S., Insteel (NYSE:IIIN) provides steel wire reinforcing products for concrete.

Insteel reported revenues of $134.3 million, down 14.7% year on year. This result came in 7.5% below analysts' expectations. It was a disappointing quarter as it also recorded a significant miss of analysts’ EBITDA and EPS estimates.

The stock is up 1.3% since reporting and currently trades at $29.87.

Read our full, actionable report on Insteel here, it’s free.

Johnson Controls (NYSE:JCI)

Founded after patenting the electric room thermostat, Johnson Controls (NYSE:JCI) specializes in building products and technology solutions, including HVAC systems, fire and security systems, and energy storage.

Johnson Controls reported revenues of $6.25 billion, up 6.7% year on year. This result missed analysts’ expectations by 14.7%. Overall, it was a softer quarter as it also logged full-year EPS guidance missing analysts’ expectations.

Johnson Controls pulled off the fastest revenue growth but had the weakest performance against analyst estimates among its peers. The stock is up 11.8% since reporting and currently trades at $83.67.

Read our full, actionable report on Johnson Controls here, it’s free.

Market Update

Thanks to the Fed's series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market has thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.