What a brutal six months it’s been for Core & Main. The stock has dropped 31.7% and now trades at $42.36, rattling many shareholders. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Given the weaker price action, is this a buying opportunity for CNM? Find out in our full research report, it’s free.

Why Are We Positive On CNM?

Formerly a division of industrial distributor HD Supply, Core & Main (NYSE:CNM) is a provider of water, wastewater, and fire protection products and services.

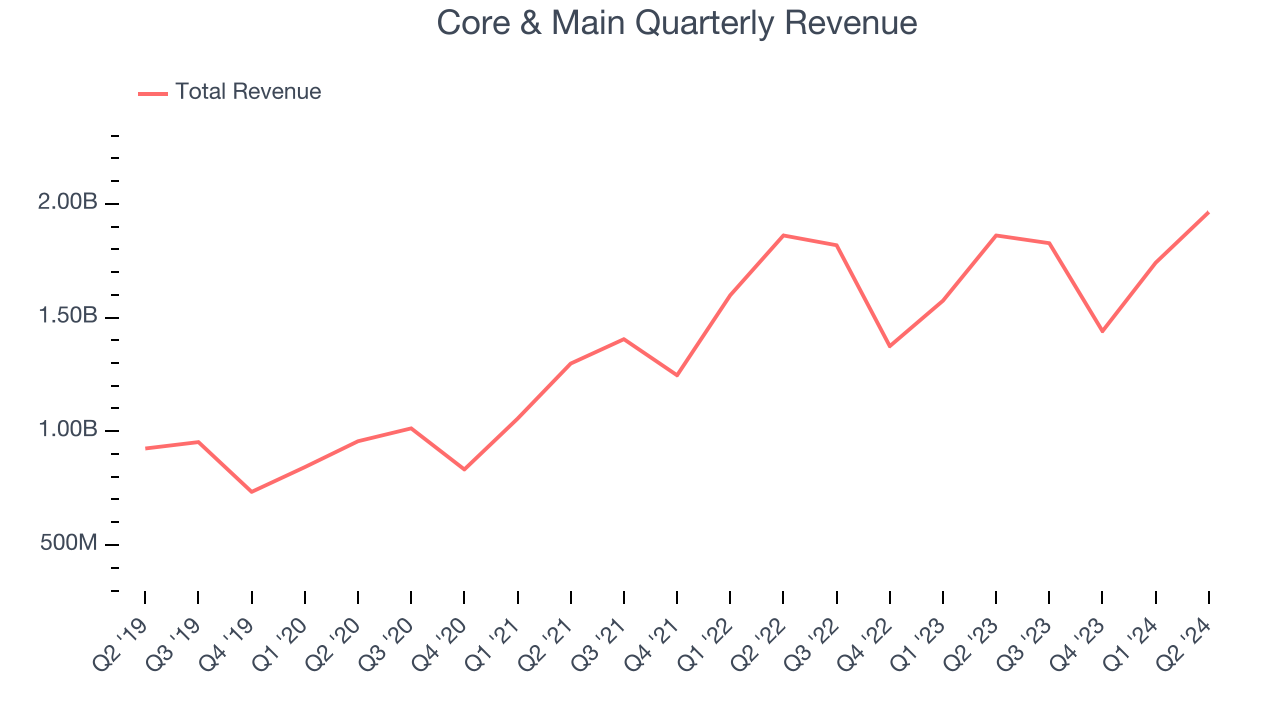

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term sales performance is an indicator of its quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Thankfully, Core & Main’s 15.5% annualized revenue growth over the last five years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers.

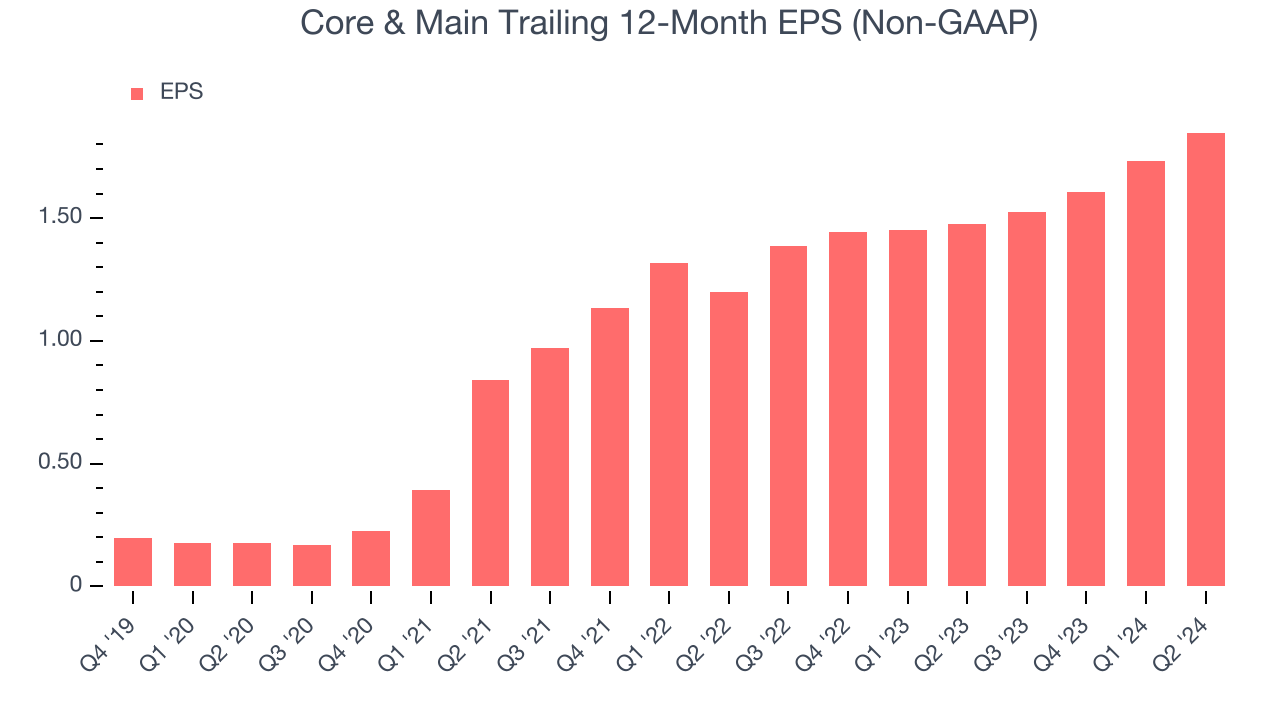

2. Long-Term EPS Growth Is Outstanding

Analyzing the long-term change in earnings per share (EPS) tells us whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Core & Main’s EPS grew at an astounding 53.3% compounded annual growth rate over the last five years, higher than its 15.5% annualized revenue growth. This tells us that after subtracting all expenses, including interest and taxes, the company became more profitable as it expanded.

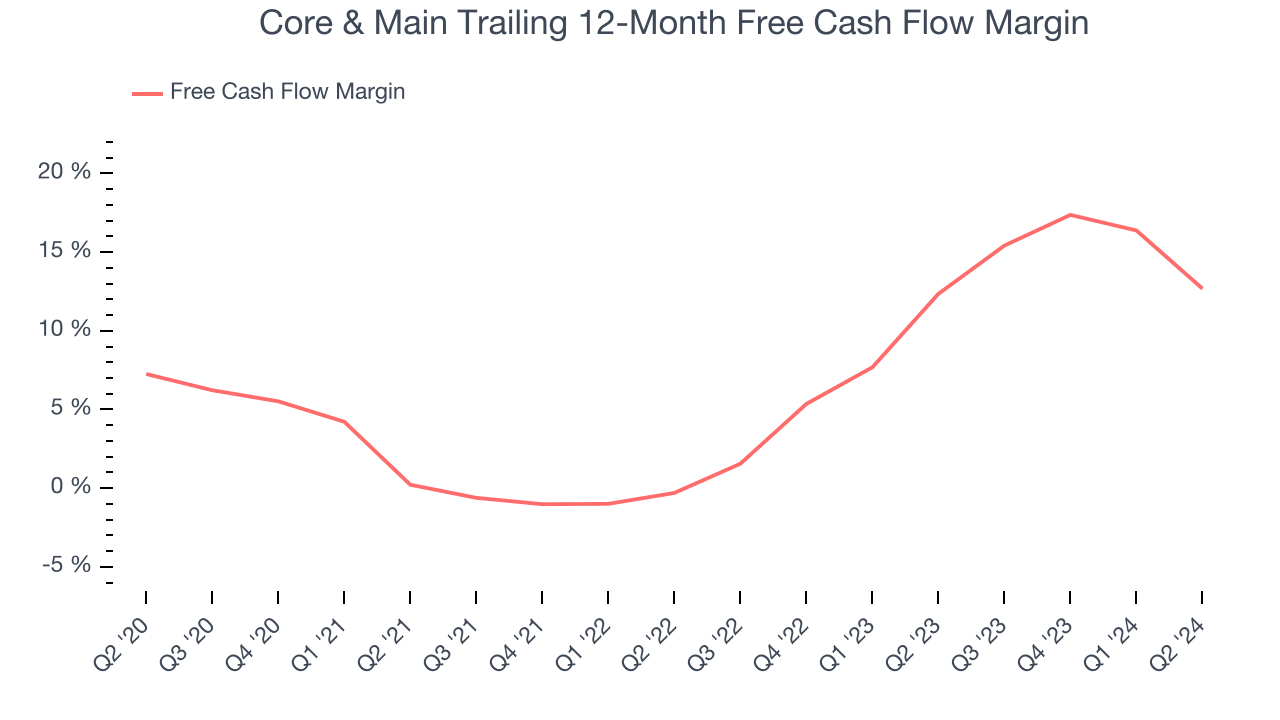

3. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Core & Main’s margin expanded by 5.4 percentage points over the last five years. This is encouraging because it gives the company more optionality. Its free cash flow margin for the trailing 12 months was 12.7%.

Final Judgment

These are just a few reasons why we think Core & Main is a high-quality business. Following the recent decline, the stock trades at 17.1x forward price-to-earnings (or $42.36 per share). Is now a good time to buy some shares? See for yourself in our comprehensive research report, it’s free.

Stocks We Would Buy Instead of Core & Main

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our 9 Best Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.